When investors evaluate the best PMS in India or the best AIF in India, the conversation usually begins with returns. Numbers like CAGR or point-to-point performance tend to dominate factsheets and marketing presentations.

While returns are important, they do not always reveal how the strategy behaves during difficult market phases.

For sophisticated portfolios, the more meaningful question is not simply how much a strategy earns, but how much it can lose along the way.

This is where drawdowns and volatility become essential metrics. Together, they reveal the risk structure beneath headline returns and help investors judge whether a strategy is sustainable over the long term.

Understanding Maximum Drawdown

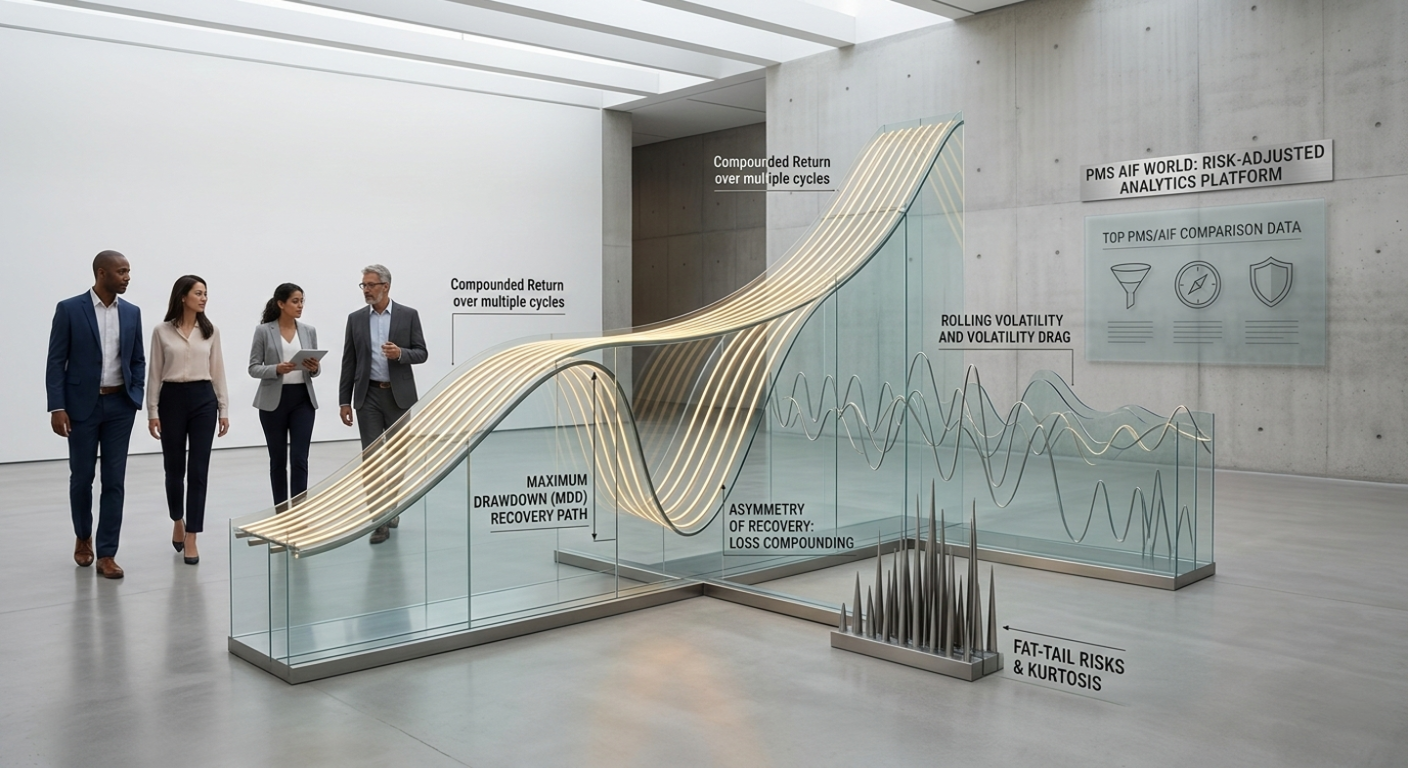

Maximum Drawdown (MDD) measures the largest decline an investment experiences from its peak before recovering to a new high. In the context of PMS and AIF strategies, this metric provides a realistic picture of downside risk.

One of the most important ideas behind drawdowns is the asymmetry of recovery. Losses compound differently from gains.

For example, a portfolio that declines by 25 percent must subsequently rise by roughly 33 percent to return to its previous value. If the decline reaches 50 percent, the required recovery jumps to 100 percent.

This mathematical reality has a direct psychological impact on investors. Even a strategy that eventually delivers strong long-term returns can become difficult to hold if the interim drawdowns are severe.

Many investors exit during market stress, which prevents them from benefiting from the eventual recovery.

Volatility as a Measure of Stability

If drawdowns measure the depth of losses, volatility measures the frequency and intensity of price movements.

Technically expressed through standard deviation, volatility reflects how widely returns fluctuate around their average.

In PMS portfolios, high volatility may indicate that a small group of stocks is driving performance. Such concentration can produce impressive returns in favorable environments but may also lead to abrupt declines when market sentiment shifts.

Lower volatility, on the other hand, often reflects diversification or a more defensive allocation strategy. While the returns may appear modest in strong bull markets, the smoother return profile can improve long-term compounding.

Volatility also introduces what analysts call volatility drag. Large fluctuations reduce the geometric return of a portfolio, meaning the actual compounded return may fall short of the average annual returns reported.

In practical terms, two funds may report similar average returns, yet the one with lower volatility often ends up delivering better wealth accumulation over time. Investors can easily analyse such volatility parameters on PMS AIF WORLD.

Looking Beyond Simple Volatility Numbers

A single volatility figure does not always tell the full story.

Professional analysts often examine rolling volatility, which measures fluctuations across multiple time windows. This helps identify whether the manager’s risk profile has remained stable or if it has changed significantly across different market cycles.

Another advanced metric is kurtosis, which measures the probability of extreme events. A portfolio with high kurtosis may appear stable most of the time, but has a greater likelihood of experiencing sharp, unexpected drawdowns.

These fat-tail risks are particularly relevant in complex AIF strategies and are increasingly tracked on research platforms such as PMS AIF WORLD.

The Importance of Recovery Time

Equally important is how quickly a portfolio recovers after a decline. Two funds might experience the same drawdown, but their recovery paths can be very different.

The concept of time to recovery measures how long it takes for a portfolio to surpass its previous peak. Top-performing PMS strategies that recover quickly often demonstrate stronger portfolio resilience and disciplined risk management.

One useful visual tool for evaluating drawdowns is the underwater plot, which shows the duration and depth of declines over time. While this specific chart format is commonly used in portfolio analysis, similar insights can also be derived from drawdown data and performance analytics available on platforms such as PMS AIF WORLD.

Wrapping Up

High returns naturally attract investor attention, but risk metrics often tell a more complete story about whether those returns can be sustained over time.

A strategy may generate impressive gains, yet if it exposes investors to deep drawdowns along the way, staying invested through an entire market cycle can become difficult.

Because for PMS and AIF investors, the objective is rarely just maximizing returns. Many investors instead look for portfolios that can deliver equity-like growth while maintaining a more controlled level of volatility.

Strategies that keep drawdowns within manageable limits often make it easier for investors to remain invested during turbulent phases, which in turn supports long-term compounding.

Seen from this perspective, drawdowns and volatility form an important part of a portfolio’s underlying structure. They reveal how a strategy behaves when market conditions turn unfavorable and help investors differentiate between temporary bursts of performance and more durable investment discipline.