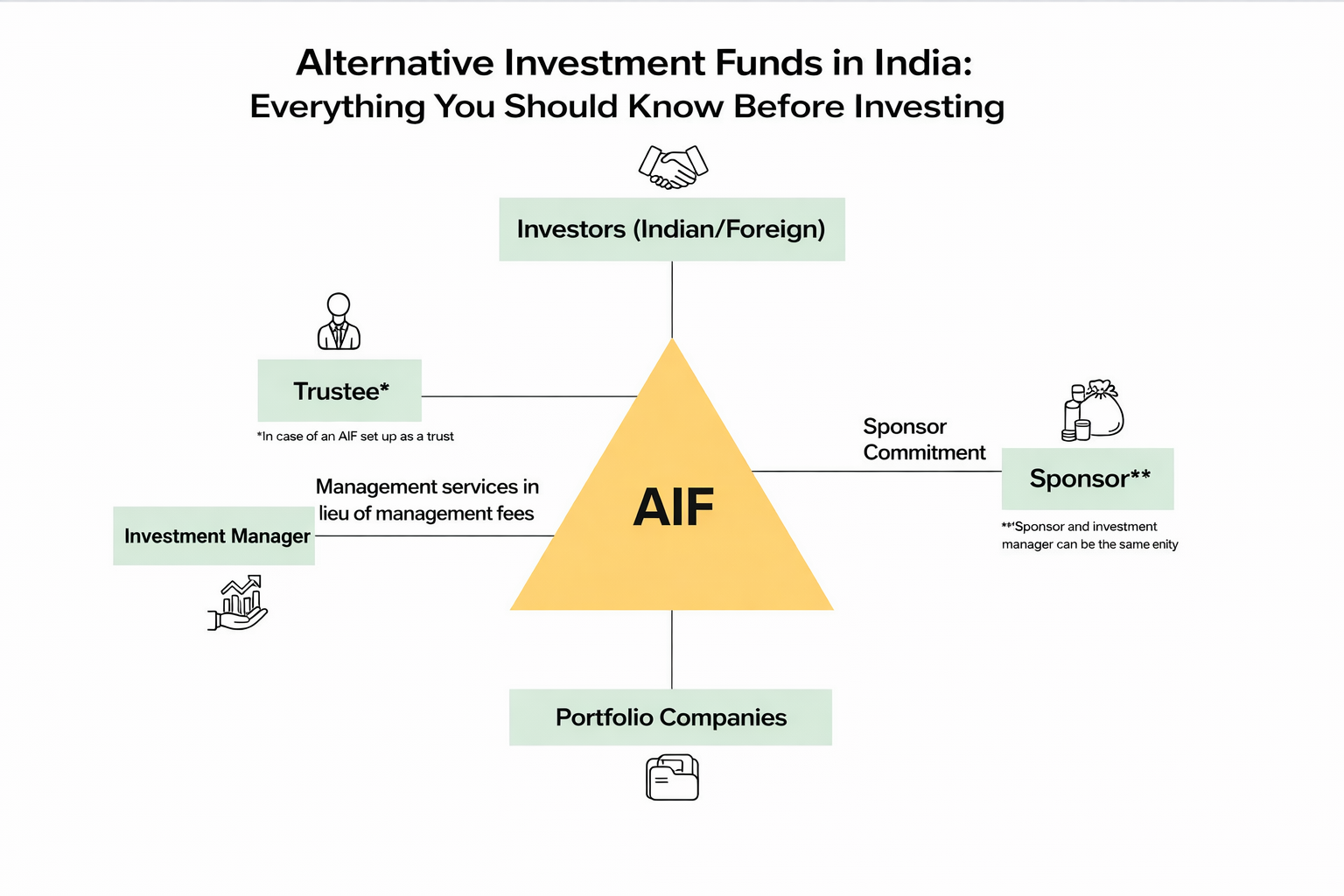

Alternative investment funds in India occupy a distinct space within the broader investment landscape.

They are not intended to replicate listed markets or track indices in a conventional sense. Instead, they provide access to private businesses, structured credit, and a set of alternative investment strategies that extend beyond what traditional portfolios typically capture.

The expansion of this segment has been gradual, though meaningful. With industry assets now exceeding ₹15 lakh crore, AIF investment in India reflects a visible shift in investor preference, away from purely market-linked returns toward more layered portfolio construction.

That said, AIFs are not uniform in how they behave. Their structure introduces certain nuances, some obvious, others less so, which are worth understanding before capital is allocated.

Understanding AIF Categories

Under SEBI AIF regulations, funds are classified into three segments, commonly referred to as AIF category 1 2 3. The classification itself isn’t complicated, but the way each category operates tends to differ in practice.

Category I AIFs focus on early-stage and development-oriented sectors such as startups, SMEs, and infrastructure. These investments align with long-term growth themes, although outcomes can be uneven, given the stage at which capital is deployed.

Category II AIFs form the more widely used segment. This includes private equity, private credit, and real estate funds. Here, investments are generally made in businesses that are relatively established, where visibility on cash flows and exits is somewhat clearer, though not without uncertainty.

Category III AIFs take a more flexible approach. Through market-linked strategies such as long-short equity and derivatives, they attempt to generate returns across different conditions. This flexibility can be advantageous, but it also introduces variability that is not always predictable.

How Capital Is Deployed?

The minimum investment threshold of ₹1 crore is often highlighted. In practice, however, the deployment structure tends to matter more.

Most AIFs follow a drawdown model. Capital is committed upfront but deployed over time, typically as AIF investment opportunities emerge. This allows funds to align capital allocation with actual opportunities rather than fixed timelines.

There is also an element of alignment within the structure. AIF fund managers are required to invest alongside investors. While this does not eliminate risk, it does ensure that decision-making is linked to shared outcomes.

Taxation

Taxation in AIFs is not uniform. It varies by category and has a direct bearing on what investors actually take home.

For Category I and II AIFs, income is typically passed through to investors. Capital gains are then taxed in the investor’s hands, depending on the nature of the asset and how long it is held.

Long-term gains, at present, are taxed at 12.5 percent.

That said, the treatment is not always straightforward. If the income is characterised as business income, the tax may apply at the fund level, often at higher rates. This usually comes down to how the strategy is structured and executed.

Category III AIFs follow a different route. They are generally taxed at the fund level itself. While this reduces the reporting burden for investors, it can weigh on post-tax returns, especially in strategies with higher churn.

Risk Realities

AIFs are often viewed through the lens of illiquidity, but the more relevant perspective is investment horizon.

In Category I and II funds, capital is tied to underlying assets that require time to create value. Lock-in periods of five to seven years are common, not as a constraint, but as a structural requirement for the strategy to work.

Category III AIFs offer relatively more flexibility. Many operate with periodic liquidity windows, and some are structured as open-ended funds. This provides a degree of access that is not typically available in other categories.

Valuation is another area that tends to be misunderstood. Since many investments are unlisted, interim valuations are indicative. They reflect progress, not necessarily realisable value. Actual outcomes become clearer at exit.

The J-curve effect follows a similar pattern. Early performance may appear muted as capital is deployed and costs are absorbed. As investments mature and exits begin, the return profile generally improves.

Regulatory Direction

The regulatory framework governing AIFs has evolved, largely with an emphasis on transparency.

Recent updates under SEBI AIF regulations have strengthened reporting standards. The Annual Activity Report (AAR) now provides investors with a more comprehensive view of fund performance and portfolio positioning.

There is also increasing participation from Accredited Investors, especially in structures that allow greater flexibility in strategy and concentration.

Overall, the direction is toward better transparency and more structured governance.

Portfolio Role

AIFs are not substitutes for traditional investments. They tend to function as a complementary allocation.

They provide access to private market opportunities, reduce reliance on public market movements, and enable exposure to specialised alternative investment strategies.

That said, allocation requires some balance. Excess exposure may constrain liquidity, while a minimal allocation may not materially influence outcomes.

Wrapping Up

The appeal of alternative investment funds in India lies in access and differentiation. These funds operate in segments that are not typically available through conventional routes.

At the same time, outcomes can vary across managers and strategies. Evaluating AIF investment opportunities, therefore, requires a degree of selectivity, with attention to consistency, risk, and broader portfolio alignment.

This is where platforms like PMS AIF WORLD add value. By focusing on consistency, risk, and portfolio construction, rather than just headline returns, the evaluation process becomes more grounded.